Cambridge, Mass.,February 5, 2020

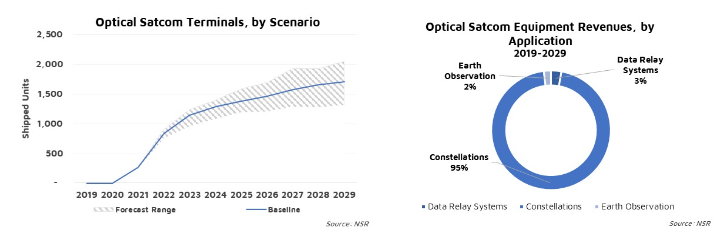

NSR’s Optical Satellite Communications, 2nd Edition report, released today, projects a $3.8 billion cumulative revenue opportunity until 2029 for space-based laser communications. The market is largely equipment-centric, with a significant portion of the revenue flow going to lasercom terminal manufacturers. Progress in this market is heavily dependent on the progress made by non-GEO constellation operators and their ability to launch and close their business cases.

Free space optical communications (FSOC) continue to remain a niche alternative to today’s radio frequency based satcom ecosystem, used primarily by governments and research organizations for demonstration missions. However, business requirements and technological maturity in recent years has spurred a new wave of interest in optical satellite communications as a potential gamechanger.

“The market for laser communication terminals (LCTs) rests strongly on the deployment of Non-GEO HTS mega-constellations, particularly if terminal prices come down,” states Shivaprakash Muruganandham, NSR Analyst and report lead author. He added, “Demand of nearly 11,000 units is expected from these constellation operators by 2029, with most of them planning to incorporate anywhere between two to five laser terminals per satellite.”

A handful of terminal manufacturers are eyeing this market, from aerospace incumbents with volume production capabilities to newer, leaner startups dependent on COTS components targeting niche adjacent segments such as commercial data relay or EO downlink services.

Earth Observation (EO) is a smaller market, with most satellite operators locked into existing RF infrastructure on the ground. “NSR recognizes the need for optical downlink capabilities for EO in the long-term, especially as sensor capabilities improve rapidly, but the optical ground segment is not yet mature for commercial viability,” adds Stella Strataki, NSR Analyst and report co-author. “Moreover, the increasing efficiency of cloud-based services for EO is expected to further constrain the market for optical downlinks”.

Many equipment manufacturers are racing to address this market with a variety of products aimed at inter-satellite links or direct-to-earth optical connectivity solutions. NSR’s report assesses the progress of key manufacturers as well as trends in the connectivity, Earth Observation, and ground segment markets. Further, NSR’s analysis highlights the growing maturity and partnerships seen in the industry value chain.

About NSR NSR is the leading global market research and consulting firm focused on the satellite and space sectors. NSR’s global team, unparalleled coverage and anticipation of trends with a higher degree of confidence and precision than the competition is the cornerstone of all NSR offerings. First to market coverage and a transparent, dependable approach sets NSR apart as the key provider of critical insight to the satellite and space industries.

Contact us at info@nsr.com to discuss how we can assist your business.

| Building upon NSR’s leading research into the space infrastructure markets, Optical Satellite Communications, 2nd Edition (OSC2) offering key insights into trends shaping the optical satcom market, the different target segments, as well as a complete assessment and forecast of manufacturing and service revenue opportunities for shipped equipment globally. NSR's OSC2 provides a clear outlook on the future of optical communications in space for all stakeholders. |

|