The latest Rethink TV forecast demonstrates the slow decline of pay TV, and the rise of the OTT market – both SVoD, and this new sector. So while the growth in SVoD that stems from the conventional TV and movie industry does more than offset the losses we see in pay TV line, what Rethink TV wanted to do was quantify ‘the other’ – long-form video content that does not originate from TV and film studios, that isn’t delivered over pay TV infrastructure, and that is often available freely to viewers.

Defining this sector has been difficult, but we chose to focus on three constituent parts – Long Form online video, Social Media video, and Gaming video. Collectively, for the purposes of this forecast, we’ll refer to them as LSG.

The research shows how LSG grows faster than SVoD, and is on track to close the gap with pay TV within a couple of decades. That event could be the end of pay TV as we know it and of course sports rights, as they de-couple from pay TV could have a huge part to play in that, and we have already published a forecast on those.

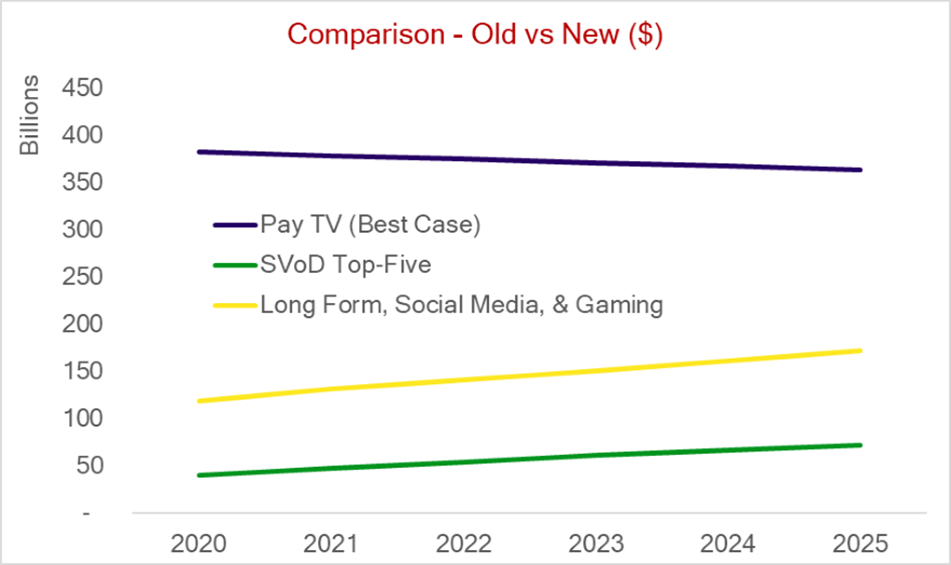

Collectively, LSG stands at around $118 billion in annual revenue currently, comprised mostly of advertising revenue, but with a sizeable chunk of subscriptions in there too. In 2025, we expect this to have grown to $171.5 billion. This compares to the aforementioned pay TV revenue of US$ 363.5 billion, chronicled in our Operator Profile database, and our top-five SVoD forecast, which grows to US$ 72.3 billion.

In 2020, pay TV revenues are around 3.2x the size of LSG, but by 2025, will only stand at 2.1x the size. In 2020, our LSG sector revenue represents 31% of pay TV, but come 2025, will have increased to be 47% of pay TV’s revenue – according to our Operator Database data and this new research. Put another way, in five years, LSG will be worth nearly half that of pay TV.

Sticking with the definitions outlined above, Long Form represents services like YouTube, Vimeo, and Dailymotion, but does include those that have some subscription tiers, such as Crunchyroll and Voot. Broadly, if you couldn’t find it in a cable TV EPG, and it is delivered online and it’s over 10 minutes long, we’re likely counting it inside Long Form.

The Long Form segment overlaps strongly with AVoD, but we are mindful of China’s influence on the numbers – due to the hybrid fashion in which its FTA options are available inside these platforms. To this end, we have broken out Tencent Video, iQIYI, Youku, and Le.com separately, which will be examined separately.

Social Media is fairly self-explanatory, and is an attempt to quantify just how much video is watched across the global social media platforms. The popularity of live video streams, from people to friends and family, as well as from businesses and personalities to their audiences, has surprised many. The length of some of these streams sometimes veers into long-form territory too, and with video still proving the most engaging content on these platforms, the more time spent here by consumers, the less time that is available to spend in the pay TV ecosystem.

Gaming is by far the smallest of the three segments that comprise LSG, but it has the most engaged audience – as you will see in our discussion of KPIs, later. It also has the fewest players, and as many of you will know, is currently dominated by Amazon’s Twitch. Of course, Microsoft has just turned this sector into a three horse race, by closing down its Mixer service and pushing its users and streamers towards Facebook Gaming. Google’s YouTube Gaming is the third player here, and while Twitch leads the market currently, its rivals have immense online platforms to leverage, to drive more eyeballs to their gaming services.

This is the latest forecast in the Rethink TV Archive, which now includes:

- Subscription VoD peaks, as Covid-19 lockdown drives sales

- How to survive the Set Top Box endgame

- Virtualization to capture 500 million fixed broadband customers by 2025

- Addressable advertising boom across all regions and platforms

-

- Esports on verge of hypergrowth to $5bn plus gambling

- SRT triggers “live” video surge – bigger than SVoD

|

|