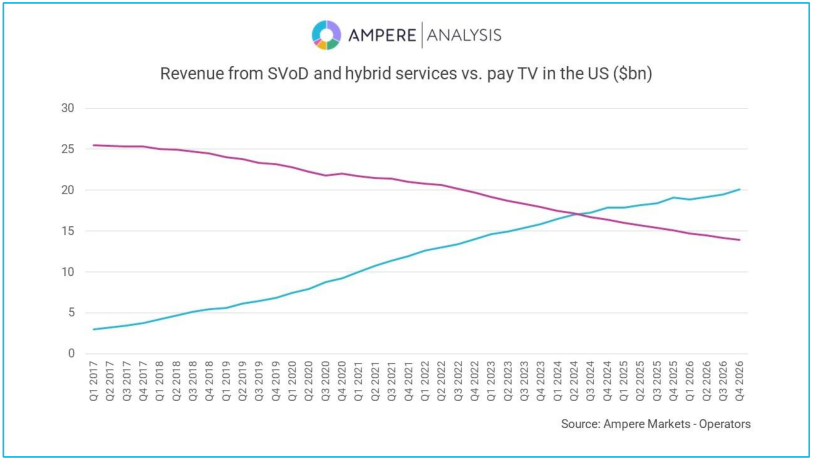

The latest research from Ampere Analysis finds that total revenues from streaming (including advertising revenue from hybrid streaming subscription tiers) will overtake revenues from pay TV subscriptions in the US for the first time in Q3 2024. Streaming will continue to race ahead as traditional pay TV declines - with the value of pay TV in 2028 expected to fall to half the value it saw at its peak in 2017. The new analysis comes from Ampere’s continuously updated Markets Operators data service.

By 2028, US pay TV revenue is expected to fall to half its 2017 peak

Streaming subs overtook pay TV in 2016, but revenue is catching up

While streaming subscriptions overtook pay TV subscribers back in 2016 in the US, streaming’s lower average revenue per user (ARPU), which currently sits at around 1/10th that of pay TV, means that revenue is only now catching up.

Streaming advertising revenues will pass $9bn in the US this year

A slowdown in the growth of subscriber numbers in markets such as the US and UK has driven a shift in focus from the streamers towards revenue growth, and eventually, profitability. As a result, the introduction of cheaper ad tiers has been successful not only in increasing new subscriber growth in previously saturated markets, but also in acting as an additional revenue source for streaming services. Revenues from ad tiers will pass $9bn in the US this year, bolstered by Amazon Prime Video’s new advertising tier which launched this quarter. Increased revenue from advertising and a boost in subscriber growth, alongside the decline in traditional pay TV, has led to this important inflection point being

reached.

.

Rory Gooderick, Senior Analyst at Ampere Analysis says: “Most major streaming services in the US have launched their hybrid advertising tiers, which, along with increasing clamp-downs on password sharing, have been successful at reigniting growth in the streaming market. There is still a way forward for pay TV, however. Disney and Charter’s recent deal in the US, which gave almost 15 million Charter subscribers access to Disney+’s advertising tier, shows how the two businesses can work together to maximise streaming’s reach to domestic subscribers, and highlights the importance of traditional distribution platforms as service aggregators. Longer term contracts and the reduction in churn makes this an attractive proposition for streamers, while control over the billing relationship also means there’s something in it for the pay TV provider too.”

About Ampere Analysis

Founded in January 2015, Ampere Analysis is a new breed of media analyst firm. The company’s experienced team of sector-leading industry analysts specialises in sport, games, pay and multiscreen TV and next-generation content distribution. Our founders have more than 60 years

combined experience of providing data, forecasts and consulting to the major film studios, telecoms and pay TV operators, technology companies, TV channel groups and investment banks. www.ampereanalysis.com