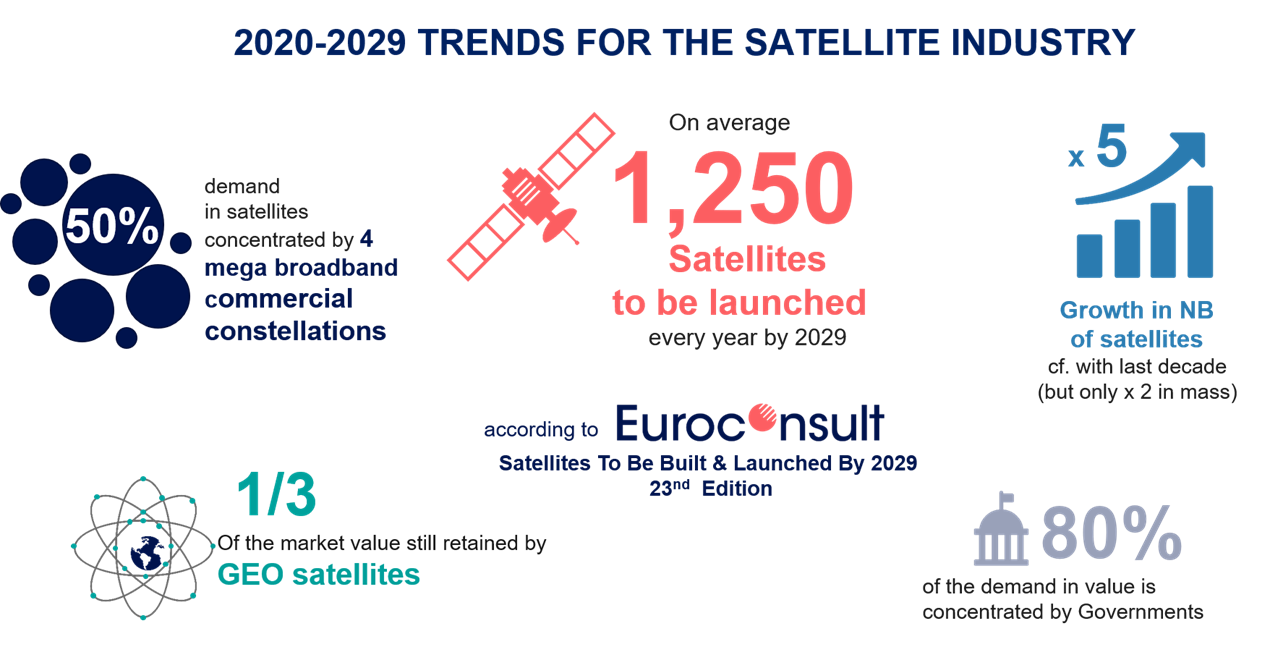

In its latest analysis of satellite manufacturing and launch services, “Satellites to be Built and Launched by 2029", Euroconsult anticipates almost a quintupling in satellite demand in the next decade with an average of 1,250 satellites to be launched on a yearly basis. In comparison to the 260 yearly satellites launched in the previous decade, this skyrocketing number cements the structural changes occurring in the market and the industry, not only in the number of satellites but also in terms of satellite missions and operators, both governmental and commercial.

“The satellite industry will indeed experience a quick and radical transformation when it comes to satellite numbers. However, despite this spike in satellite demand, we are looking at half of the market concentrated around a handful of mega constellations. In addition, some being vertically integrated means that their procurement will not be done on an open competition basis. Nevertheless, GEO comsat remains the leading segment pulling 1/3 of the market revenues, but here too we anticipate -20% drop in operational assets by 2029.” argued Maxime Puteaux, Editor-in-Chief of this research product and Principal advisor at Euroconsult. Several key market trends are catalysing the satellite industry’s structural changes:

- For the first time in a single year more than 1000 satellites were launched, of which 70% from Starlink alone. This symbolic threshold will become a new standard for the next ten years with significant annual variations mainly driven by the replacement of the commercial constellations.

- The orders of GEO comsat have been exceptionally high in 2020 at 18 units, of which 13 for the accelerated C-band clearance plan of the FCC in the USA. In addition, proof of a structural slowdown of that market in satellite numbers, GEO comsat replacement is also challenged by fleet rationalization approaches, in-orbit life extension and transitioning of some of the traffic to upcoming NGSO constellations. Manufacturers’ GEO comsat product portfolios are diversifying, ranging from a few hundred kilograms to 6 Tons VHTS. Digital payloads become the rule for a data-centric market (rather than a broadcasting market).

- Beyond the “commercial space” momentum, governments will remain the first customers with 80% satellite manufacturing and launch revenues for the period. Investments by defence operators is driven by security applications and a growing endorsement of smallsats, COTS and constellations while civil agencies focus on large Earth observation systems.

- Access to the space industry is diversifying with a few smallsat-dedicated launchers now operational and more expected to perform maiden flights in 2021. A new generation of GTO-capable launchers is expected to enter the market within the next two years with a design-to-cost approach. Meanwhile, SpaceX masters reusability and executes Starlink’s launches at marginal cost, with Falcon 9 recovery and reuse becoming a standard endorsed by customer.

About this research

The 23rd edition of "Satellites to be Built & Launched by 2029" provides an in-depth analysis of the status and future trends of the global demand and supply distribution for satellites over the next 10 years, whilst detailing market drivers and technology evolution. In its analysis, Euroconsult reviews strategic issues and trends by type of satellite operator, orbits, region of the world and application. It provides a quantitative analysis of satellite numbers, mass, and cost with forecasts based on qualitative top-down and bottom-up assessments. With separate sections for both the manufacturing and launch industries, the research covers strategic issues, industry structure, financial performance, innovation and includes detailed profiles of seventeen top satellite manufacturers and launch service providers.

“The 2020 edition will help our clients navigate this fast-changing environment. With this new edition of our flagship research, we have looked beyond number forecasts to provide insights into the GEO comsat replacement cycle and deliver constellation maturity and credibility assessments. We also monitor new government programs, M&As and venture capital investments and technology evolution, whilst refining our price and CAPEX modelling for a more accurate predictive analysis.” Maxime added.

“Satellites to be Built & Launched by 2029” is available now and can be ordered from the Euroconsult shop. A sneak-peak free extract of the research is also available here.