NSR’s newly released Cloud Computing via Satellite, 3rd Edition sees Cloud Service Delivery via Satellite positioned to generate US$ 32 Billion, with 240+ Exabytes of Traffic, by 2031. The impending wave of LEO, MEO, and GEO-HTS satcom and data services is set to boost long- term cloud adoption, significantly enhancing market engagement opportunities.

Going forward, Cloud will play a key role in bridging gaps between traditional upstream aerospace/satellite players focused on manufacturing spacecraft and launching into orbit, and downstream end users and middle layer organizations, where demand resides.

“With the need to address user-specific requirements across verticals, Cloud solutions adoption is expected to increase,” states report co-author Shivaprakash Muruganandham. “Cloud-hosted applications, cloud storage/processing by geospatial analytics providers, and direct cloud connectivity for satcom will all further growth in this market, evolving business models development.”

New partnerships and service roll out offer market capture and growth potential, as satellite players vie to capture the untapped addressable markets across verticals, from communications to data downlink and geospatial analytics.

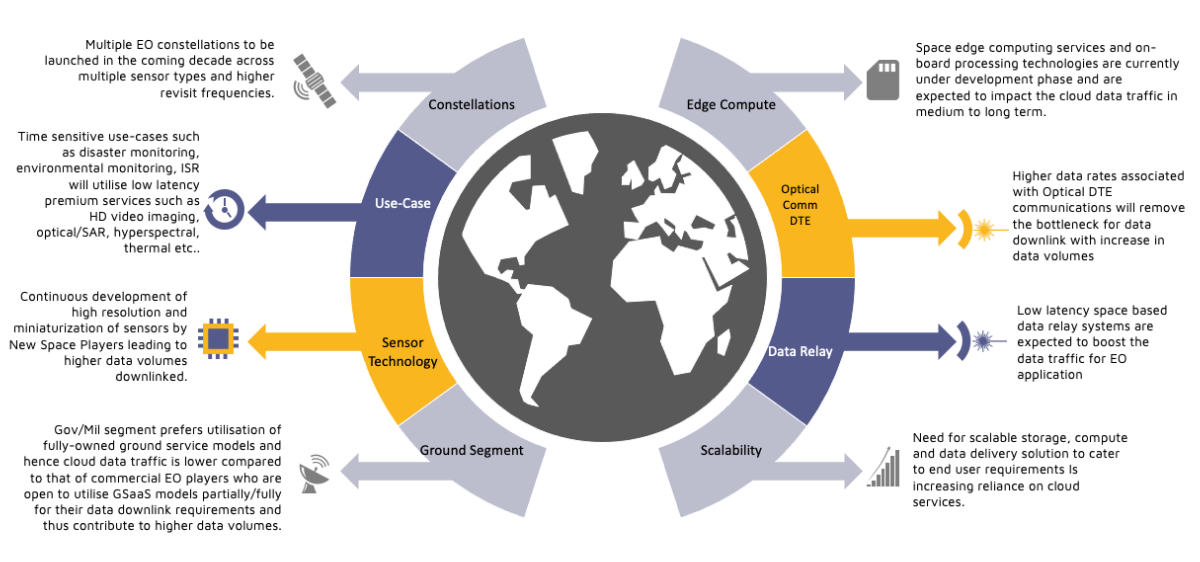

“The market for data downlink onto cloud servers towards EO applications is growing significantly,” notes report co-author Prachi Kawade. “Driven by an increasing number of constellations and increasingly rich information driving toward higher volumes, particularly with HR and VHR data, be it SAR, hyperspectral or sub-meter resolution optical imagery, opportunity is set to broaden.”

While 98% of data traffic come from satcom cloud services, volume is growing for Earth Observation, Situational Awareness and science applications as large cloud and IT players make further in-roads into traditional satellite industry, shaking up the market ecosystem.

Muruganandham concludes, “Cloud adoption is lowering the barriers to entry for space-derived data services, especially on the downstream side of the market. With greater opportunities available to them than in the past, today’s start-ups born in the cloud are shaping the future of the satellite industry.”

|

|

|

|

|

|

NOW AVAILABLE

Cloud Computing via Satellite,

3rd Edition

|

|

|

|